In our July ratings, a more nuanced pictured emerged for Japanese companies. The significantly positive correlation of financial performance with the percentage of INEDs and the number of Female Directors disappeared this month, suggesting that an increasing number of non-superior performers are “copying” other companies in this respect, and/or have only only done so recently so no positive impact (should there be any) is discernible.

Tag: Corporate Governance Code

METRICAL: CG Top 20 stocks slightly underperformed in May… and a focus on board chairs

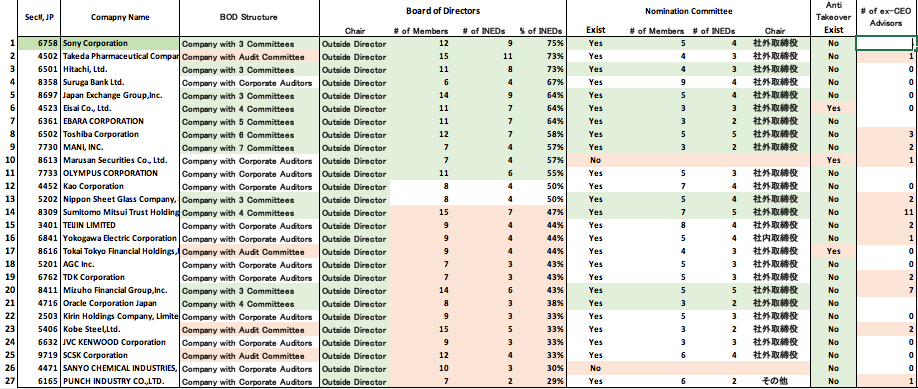

Chair of the Board of Directors

We would like to highlight the function of the chair of the board. Of about 1,800 companies, only 27 companies are chaired by an outside director. This indicates just how resistant inside directors are in entrusting the position of chair of the board to an outside director. The table below shows the 27 companies.

Corporate Governance in Japan: What Has Changed in the Past Three Years?

I recently gave a presentation in which I tried to answer this question. Here are the top-line conclusions:

- Investors are finding their voting voices

- Now they need to find to find their asking voices

- There is a way to tear down the “allegiant shareholder ” wall

- Factors that correlate with superior performance include: >= independent directors, low “allegiant” holdings, >15% female directors, and age of firm <45 years

- Activism is becoming more effective

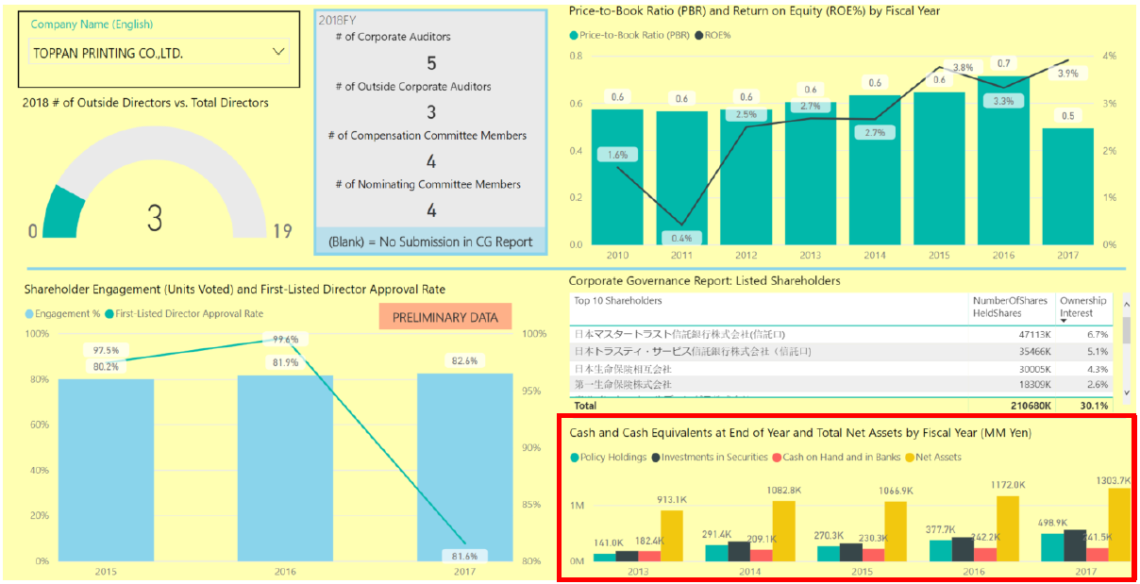

These conclusions are based on a huge amount of time-series data we have collected. We are now building a comprehensive time-series database that includes not only financial data, but all text and numerical data from financial reports and CG Reports, as well as tabulated AGM voting results for each resolution. The data will be organized so that one can zero in on exactly the data one needs. Here is a simple example showing board practices parameters, historical AGM participation and CEO approval rates, and the trend of ownership of “allegiant shareholdings”:

Japan’s Corporate Governance Conundrum, and How Investors Can Solve it

Out of more than 700 defined-benefit corporate pension plans in Japan, only five non-financial corporate pension plans have signed the SC. Second, a major portion of Japan’s asset owners are the companies themselves, in the form of direct “policy holdings” of the shares issued by other companies. Japan’s dual walls of “conflicted pension governance” and “allegiant shareholders” need to be torn down. Here is how it can be done.

How to Demolish Japan’s Wall of Yes-Man Allegiant Shareholders

By Nicholas Benes

The short story: it will not be so hard if institutional shareholders really want to topple it, and use the technique suggested here. But first, the background.

Background

This is still the biggest defect of Japan’s equity market, and recent reforms have only made a small dent in it. At the average listed company, between 35% and 50% of the stock is owned by such holders if one includes not only firms in “cross-shareholding” relationships but also firms that unilaterally hold stock in order to win business; most holdings by

banks and insurance companies; and parent companies, subsidiaries, and affiliates. Consistent with this estimate, when Japanese listed companies were asked, “what percent of your shareholders can you count to support management?” in late 2017, fully more than two-thirds of companies responded with numbers in the 30-60% range.

These “policy holdings” by “stable shareholders” represent a massive misallocation of capital that is being put at risk largely for the purpose of protecting executive teams at other companies. In 1967, Japan’s one of Japan’s most venerated managers and the founder of Panasonic, Konosuke Matsushita, minced no words in noting his concern about the then-recent rise of “stable” cross-shareholdings in these words: “If this situation continues, I think it is in no way desirable, because of the risk that once again a maldistribution of capital in our country will occur. I believe that this is not a sign of progress in capitalism; rather, it should be considered as a sign that we are moving backwards.”

The Story Behind Japan’s Corporate Governance Reforms

Frequent visitors to our blog are likely aware of Japan’s major corporate governance reforms, but not everyone is familiar with the story behind how these reforms were crafted. The eminent Steven K. Vogel (Professor of Political Science at the University of California, Berkeley), recently wrote a concise and easy-to-follow history of the major reforms to Japanese corporate governance practices since the 1990s, describing how and why they came to pass.

Public Comment to the METI Fair M&A Study Group (by Nicholas Benes)

As the person who initially proposed the Corporate Governance Code to the LDP in 2013 and 2014, I am well aware of its limitations in various areas. For this reason, I am very pleased that Fair M&A Study Group have decided that its discussions should cover not only MBOs, but also ”cases which are likewise significantly affected by the issues of conflict of interest and information asymmetry”[1], including “cases of acquisition of a controlled company by its controlling shareholder.”[2]

This indeed an important mission, because these topics include virtually all types of M&A transactions and the public statements of executives and boards with regard to them. For many years in the post-war era, the failure of the government and the JPX/TSE to set forth clear bright-line rules that facilitate a fair, robust M&A market in Japan has stunted productivity, dynamism and growth in the Japanese economy.

“Linkage Between Corporate Governance and Value Creation” (METRICAL/BDTI) – Update as of January, 2019

Our joint research – “Linkage Between Corporate Governance and Value Creation” – between BDTI and METRICAL has been updated as of January 31. The most important inferences are summarized below.

(1) Correlations: Board Practices

and Performance

Significant correlation between board practices and performance continues.

(a) ROE: Nominations Committee existence, the number of female directors and percentage of INEDs show a significant positive correlation.

(b) Tobins Q: Nominations Committee, retired top management “advisors” (ex-CEO “advisors”), and percentage of INEDs show

(c) ROA (actual): Compensation Committee existence (negative correlation), Incentive Compensation Plan disclosure, and retired top management (ex-CEO) serving as advisors show significant correlation.

Amended, Detailed Public Comment by Nicholas Benes to JPX re: “Review of the TSE Cash Equity Market Structure”

NOTE: This public comment supersedes and replaces the one that I, Nicholas Benes, submitted on January 12, 2019)

As the person who initially proposed the Corporate Governance Code to the LDP in 2013 and 2014, and suggested a number of principles in it, I am well aware of its limitations in various areas and the fact that Japan has not yet attained the quality level for an equity market that is expected by global investors. In this sense I am very pleased that the JPX has decided to review its equity market structure and related standards.

Challenges and Realities

This indeed an important mission, for which is it essential to recognize and discuss the impact of a number of challenges that Japan faces in improving governance, efficiency, and trustworthiness of its equity capital markets. These challenges include:

Engagement in Japan: How to Discuss Director and Executive Education – the Most Necessary Thing!

Executive training is badly needed in order for independent directors to perform their expected role

When I proposed to the LDP and the government in 2013 that Japan promulgate a corporate governance code, one of the most important principles that I advised should be included in it was a requirement for director and pre-director training. To anyone who has ever sat on an average Japanese board, the need for this is obvious. Without more training of both executives and external directors in Japan, it will continue to be very difficult for independent directors to perform the roles that are now expected of them. From personal experience, I know that it is simply not possible to convince engineers who do not understand finance that their company could very easily go bankrupt in two years.