On July 12, 2019, I gave a presentation about Work Style Reform in Japan at a seminar organized by the Japan America Society of Washington DC in the beautiful meeting room of the Groom Law Group. The talking points in my presentation were the background of the reform (political background and male dominated office), the major points of amendment to laws, the problems and keys to improving productivity, the young generation’s view of employment activity and work-life balance, protection for non-regular employees, and some implications to businesses in Japan. The questions and opinions raised by the participants were as follows.

Category: Law

Public Comment to the METI Fair M&A Study Group (by Nicholas Benes)

As the person who initially proposed the Corporate Governance Code to the LDP in 2013 and 2014, I am well aware of its limitations in various areas. For this reason, I am very pleased that Fair M&A Study Group have decided that its discussions should cover not only MBOs, but also ”cases which are likewise significantly affected by the issues of conflict of interest and information asymmetry”[1], including “cases of acquisition of a controlled company by its controlling shareholder.”[2]

This indeed an important mission, because these topics include virtually all types of M&A transactions and the public statements of executives and boards with regard to them. For many years in the post-war era, the failure of the government and the JPX/TSE to set forth clear bright-line rules that facilitate a fair, robust M&A market in Japan has stunted productivity, dynamism and growth in the Japanese economy.

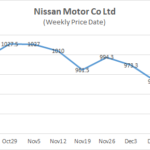

Damages Estimation- How Much Will Nissan Have to Pay to Investors?

Mr. Ghosn’s criminal cases are ongoing. But the criminal cases alone will not put a close to this entire ordeal. It is a matter of time for Nissan to face civil cases filed by investors. Due to Mr. Ghosn’s understated compensation, it is anticipated that a considerable amount of assets will flow out of Nissan. The largest part of this outflow will be accounted for the damages claimed by and awarded to investors in civil lawsuits. What amount of assets will flow out of Nissan? This memo is an attempt to estimate the probable size of these damages.

Company Law Reform in Japan: Losing its Mojo?

by Nicholas Benes

This year, Japan’s governance reform drive will either keep going, or run out of steam. Judging from the amendment of the Company Law that is now underway by an advisory council of the Ministry of Justice (MOJ), the latter is likely.

Strikingly absent is a clear over-arching vision of the most important themes that amendment of the Company Law should address now that the country has a corporate governance code. In other words, what is missing, that can only be addressed via the Company Law?

If the government were truly intent on bringing about behavioral change on the part of all Japanese boards and executives, it would focus on harmonizing key aspects of the confusing array of three different corporate governance models which listed companies can adopt, and moving towards a more consistent version of the “monitoring model” for governance that has become internationally accepted and is now embodied in its own corporate governance code.

To do this, it would change the law to enable boards to flexibly appoint capable (and legally accountable) senior executives from a much wider range of candidates than is currently possible. It would also establish rules that require boards to fulfill the independent supervisory and oversight roles envisioned for them under the corporate governance code, unaffected by managerial self-interest, if they wish to delegate wider authority to executives and pay them incentive compensation determined solely by the board.

Japan’s Revised Stewardship Code Now Requires Disclosure of Voting Records, in Principle

The FSA has finalized its revision of the Stewardship Code. Perhaps the biggest change is that it now encourages signatories to disclose their voting records “for each investee company on a per-agenda basis”, something I proposed to the FSA in 2010 but was ignored. However as you can see below, this is a “comply or explain rule”, thus weakening it to some extent:

“Institutional investors should disclose voting records for each investee company on an individual agenda item basis. (If there is a reason to believe it inappropriate to disclose such company-specific voting records on an individual agenda item basis due to the specific circumstances of an investor, the investor should proactively explain the reason. Institutional investors should at a minimum aggregate the voting records into each major kind of proposal, and publicly disclose them.)”

Top Ten International Anti-Corruption Developments for September 2016

On November 22nd Morrison & Foerster LLP made public their latest legal update titled “Top Ten International Anti-Corruption Developments for September 2016”.

In this update they summarize “some of the most important international anti-corruption developments from the past month, with links to primary resources.” This month they ask: “What is a Department of Justice (DOJ) “declination with disgorgement”? How many FCPA resolutions was the Securities and Exchange Commission (SEC) able to bring in the last month of its fiscal year? How does one avoid running afoul of South Korea’s new anti-corruption laws?”

Japanese Minority Shareholder Cash Out Transactions — Supreme Court Decision on Share Price (Jones Day Tokyo)

On July 1, 2016, the Supreme Court (first petty bench) issued a decision (the “Decision”) that may have a material impact on Japanese M&A practice.

The Decision involves the determination of the price for callable shares (zembu shutoku joko tsuki shurui kabushiki) redeemed by a target company to cash out minority shareholders after a tender offer by an acquirer.

GPIF Sues Toshiba: Japan’s Securities Law that Makes it Easy to Sue

The the news of the day is that GPIF is suing Toshiba for $10 million. It is only one asset manager that is suing, almost certainly under Article 21-2 Japan securities law (FIL) which makes it very easy for plaintiffs to sue and claim a “presumed damages amount”, and then shifts the burden of proof to the defendant company (unlike US law) to disprove its negligence. The stock has come down by about 26% or so. (Interestingly, Japanese securities law in this area is much harsher than US law, which never shifts the burden of proof in such cases.)

Prof. Sean J. Griffith: ”Corporate Governance in an Era of Compliance”

”Abstract: Compliance is the new corporate governance. The compliance function is the means by which firms adapt behavior to legal, regulatory, and social norms. Formerly, this might have been conceived as a typical governance matter to be handled at the discretion of the board of directors. Compliance, however, does not fit traditional models of corporate governance. It does not come from the board of directors, state corporate law, or federal securities law. Compliance amounts instead to an internal governance structure imposed upon the firm from the outside by enforcement agents. This insight has important implications, both practical and theoretical, for corporate law and corporate governance. This Article pairs a detailed descriptive study of the contemporary compliance function with a normative account of its incompatibility with current conceptions of corporate governance. It argues that compliance alters the political economy of American business, challenges governance efficiency, and makes old theories of the firm new again. Prescriptively, the Article calls for greater transparency and a more limited role for government in designing corporate governance mechanisms………”

”MMC’s culture of disregarding legal compliance behind data falsification”

The Yomiuri Shimbun:

”Mitsubishi Motors Corp. was found to have manipulated data to overstate the fuel economy of minicar models.

Fuel efficiency is an important element for consumers to consider when they buy cars. Falsification of such data is an extremely malicious act.

MMC overstated the fuel economy by 5 percent to 10 percent by intentionally underestimating figures concerning tire resistance and other resistance while the vehicles are in motion.