Japan Only Needs One Governance Format for Listed Firms, Not Three

- No Other Major Country Has Three Different Governance Formats

- “Three” Leads to Confusion and Uninformed, Inefficient Engagement

- Revision of the Companies Law is a Perfect Opportunity for Convergence

Limitations of Being “Unique Japan”

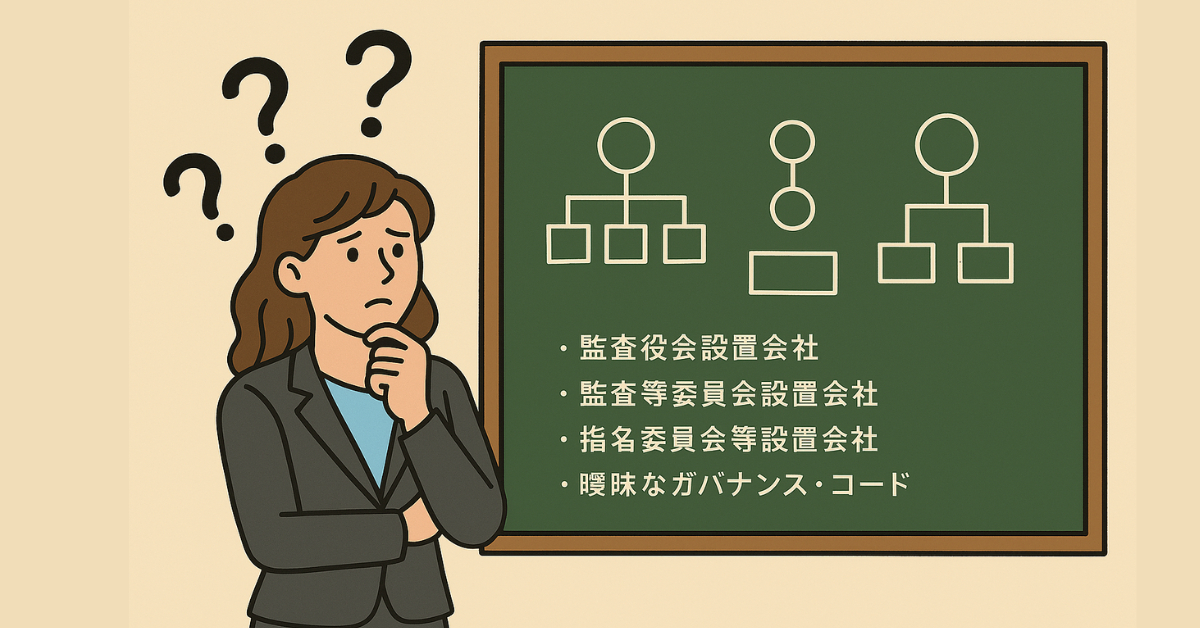

As many readers know, listed companies in Japan can choose from three different types of legal governance formats set forth in the Companies Act. The first is the traditional model with non-voting “corporate auditors” (kansayaku), the second is the “three-committee” or “company with a nominating committee” system adopted in many other countries (but rarely used in Japan), and the third is the “audit committee” system that has become popular in recent years.

Because other countries do not allow listed companies to choose from this variety of different governance structures, Japan’s market seems odd and cumbersome to foreign investors. This is because the original purpose of governance formats is not only to facilitate effective governance, but also to enable investors to compare and analyze companies on a consistent basis, and then to interact with them efficiently.

As for Japanese investors, most of them have long since given up questioning whether it is wise for there to be three separate formats.

This is a shame, because having three different “governance designs” creates great confusion among both management and investors. In many cases, the differences, advantages, and disadvantages of each design are not fully understood, and it is often difficult to grasp the real reason why a company has changed from one format to another. Although boards of directors spend much time during the implementation phase, naturally a newly adopted structure does not always function well from the start. Investors may fail to understand the company’s explanations for the change, or demand a change to a different design based on insufficient understanding.

As a result, dialogue between companies and investors regarding governance practices is not efficient. A lot of time is spent trying to understand the legal governance structure adopted by a listed company and confirming the unstandardized practices that the firm has tacked on top of that “base”, – a process that is frustrated by insufficient knowledge on the part of investors. In the worst case, investors and managers alike may think that they will learn the finer points when they need to, but by the time they need to, it is too late.

The background to this situation is the political process by which the Companies Act has been consecutively amended every 10 years or so. Whenever institutional investors have requested specific reforms, METI has introduced a new structure rather than modifying an existing framework. Moreover, at each juncture the Ministry of Justice (MOJ) did not fully consider the convenience of investors and the need to make Japanese corporate governance easier to understand. In retrospect, to them the law was a topic for lawyers, academics and corporations to refine, not investors. As a result of this approach, – or rather, you might say that this was one implicit goal driving things – the companies that resisted governance reform the most now have three different coexisting governance formats to choose from, but did not need to change their own governance structure and practices at all.

Although I teach about the three governance formats in training programs at my organization, The Board Director Training Institute of Japan (BDTI, bdti.or.jp), it is difficult to cover all of the detailed differences, issues, and informal practices that relate to each structure. It is time consuming and much of what is explained may not be currently relevant to a particular student. The result is inefficiency, and frankly laziness, in the process of simply learning about the three structures. To a Japanese person being taught, the topic is often sort of a confusing bother. It leaves many foreigners shaking their heads.

The magnitude of complexity often feels greater than simply multiplying by three. A few specific examples will help the reader understand.

- In some structures, nominations and compensation committees are legally required to be formed and to function, while in others such “committees” are only “advisory committees” formed on an optional basis, with the board of directors making final decisions,… and with no rules for their operation and composition.

- Some designs allow broad decision-making authority to be delegated to executives, but only one design allows all executives to be held accountable via shareholder derivative lawsuits.

- The “Audit Committee” required by one structure also has the right to express its opinion on nominations, but its opinion is not binding. This feature is not included in the other designs.

If you ask five executive directors and five fund managers about the difference between an executive director and an executive officer, the difference between an “independent decision-making” system(独任制) and “group decision-making”(合議制), or whether the decisions of a [specific company’s] committee are binding on the board of directors, the percentage of correct answers would probably be less than 30 percent.

Amendment of the Companies Act is an Excellent Opportunity for Convergence

This year and next, the Ministry of Justice’s Legislative Council will be discussing revisions to the Companies Act, and the Financial Services Agency will revise the Corporate Governance Code (CGC). This is an excellent opportunity to consolidate the three corporate governance structures adopted by listed companies into a single one. (Of course, if this were done, for non-listed companies the existing formats could continue to be used, and and any changes towards convergence could be made in later on, in stages.)

Unification into a single governance structure would allow the FSA to draft a more readable revised CGC, setting forth in shorter, clearer sentences the best practices that should be standardized. The need for the FSA to write long, vague sentences in order to accommodate three separate designs would be eliminated, reducing confusion and allowing dialogue with investors to focus on more meaningful topics.

Just like the “integrated disclosure” now being discussed for business reports and annual reports, such “integration” or “convergence” is absolutely essential from the perspective of governance reform. The purpose of corporate governance is to optimize “direction and control,” especially in public companies, and to create organizations that promote open discussion and debate, an atmosphere of healthy tension, and accountability for the benefit of shareholders and society. It is not to confuse investors by making it harder to compare companies and the accountability of executives. Rather than aiming to maintain the current “comfortable” designs that arose over time, the top priority should be to achieve effective governance and comparability.

At this point in time, the Ministry of Justice does not have such an ambitious plan. However, it is of utmost importance to Japan’s market to promote consolidation, lest it forever be viewed as the market in Asia that could never fully modernize itself.

In the end, the voices of powerful institutional investors, combined with political leadership, will almost certainly be necessary. Japan’s bureaucrats are very capable, but they cannot get major changes like this started. It is too risky for their careers.

Nicholas Benes

September 22, 2025

P.S.

For clarity, – I do not believe that the current “three-committee” (3C) structure should be used “as is” as the base for consolidation. I believe that the shortcomings of the existing 3C design should be corrected first, and after an appropriate degree of flexibility is added to the design, the required format for listed companies should then be set forth based on that new design. For example, to refine the 3C structure and make it more flexible, I think it is necessary to (1) establish a definition of “independence” in the Companies Act and (2) establish a rule that the decisions of the nominations committee are not binding on the board if the majority of directors are independent directors. Also, it goes without saying that transitional measures should be established so that whatever changes are made, can be put in place over a period of years.